On June 11, NOAA's National Weather Service confirmed that El Niño has developed in the tropical Pacific. NOAA also put a 63 percent probability on the event reaching very strong intensity, meaning sea surface temperatures more than 2 degrees Celsius above normal. For aquaculture, that second number matters more than the first. El Niño arrives every few years and the industry has adapted to it. A very strong El Niño is a different problem, and the last few times sea temperatures reached that threshold, Peru's anchovy fishery took the hit.

Why Peruvian anchovy is the pressure point

Peru's north-central anchovy fishery supplies roughly 20 percent of the world's fishmeal and fish oil. When water off the Peruvian coast warms sharply, anchovy schools move deeper and disperse, and the juvenile share of what's left near the surface rises. Peru's government manages this by closing or delaying fishing seasons rather than letting boats catch through it, since juvenile catch this early damages the following year's stock.

That management approach protects the fishery, but it also means supply disruption becomes the default response to a strong El Niño, not a possible one. As of June 11, Peru's Ministry of Production had already extended fishing restrictions in the north-central zone due to warm water and high juvenile presence, with no confirmed date for the season to resume. NOAA's outlook has El Niño peaking in the fourth quarter, so the restrictions are more likely to extend than lift in the near term.

This isn't the fishery's first strong El Niño. In 2023, Peru's first anchovy season was cancelled outright and the second closed early, a stretch industry observers called the worst in decades. The fallout: more than $1.4 billion in lost fishmeal and fish oil export sales, a 17 percent drop in fishing sector income, a 0.5 percent hit to Peru's GDP, and roughly 18,000 fishermen without income for most of the year. That's the scale of disruption a single very strong El Niño can produce in this fishery alone.

Prices are already moving

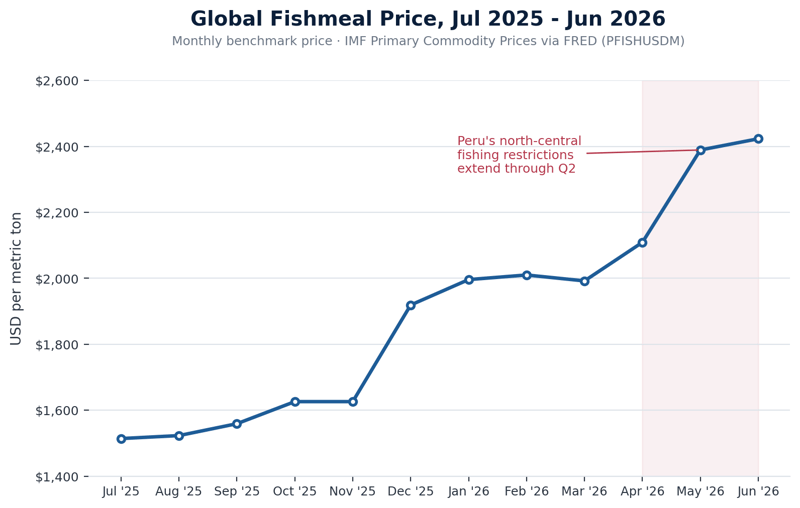

The current season's disruptions are already showing up in fishmeal pricing. IMF benchmark data puts the global fishmeal price at $1,626 per ton in October 2025, before the current restrictions began. By June 2026 that figure had climbed to $2,423, with the steepest part of the move landing between April and June, the same window Peru's north-central fishing bans extended repeatedly.

Fish oil has followed a similar trajectory, tightening alongside fishmeal as the same restricted catch limits both products at once, since anchovy is the shared raw material behind them.

None of this is happening in isolation from the rest of aquaculture's cost structure, either. Rabobank's research has projected that fishmeal could face a structural supply shortage as early as 2028, with fish oil scarcity intensifying steadily through the rest of the decade. That's a demand problem layered underneath a supply shock: aquaculture already consumes roughly 90 percent of the world's fishmeal and 65 to 70 percent of its fish oil, and that share is not shrinking. A strong El Niño doesn't create that gap, but it pulls a multi-year structural trend forward into an immediate pricing event.

Shipping adds a second layer of cost

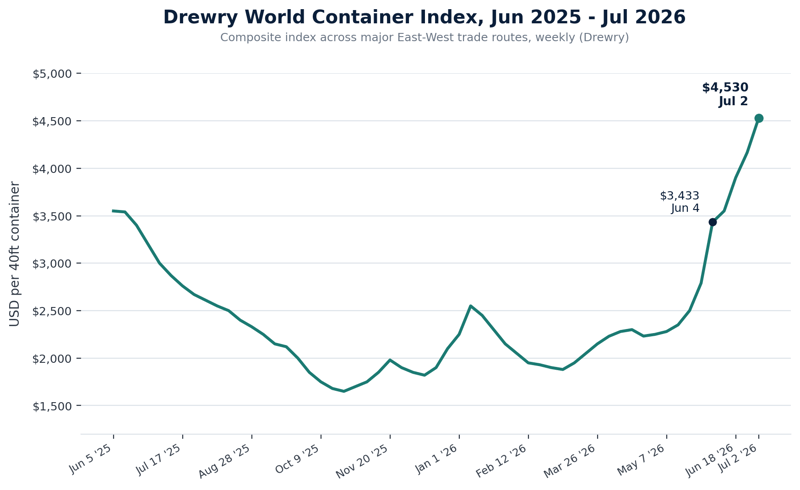

Feed ingredients also have to move, and that part of the supply chain is under its own pressure. The Drewry World Container Index, a benchmark for global container shipping rates, was sitting near $3,433 per 40-foot container in early June, close to levels last seen during the COVID and Ukraine war disruptions. The immediate driver is the conflict involving Iran: rates on the Transpacific and Asia-Europe routes have climbed sharply since the war began in late February, largely on spiking bunker fuel costs, with spot rates on some Asia-to-US routes roughly doubling over that period. The index kept climbing after that, reaching $4,530 by early July.

Fish oil and fishmeal produced in Peru still have to reach aquafeed manufacturers, and container costs are one more input getting more expensive at the same time raw material supply is getting tighter.

Why this combination is different

Any one of these pressures has shown up before. The industry worked through a very strong El Niño in 2023. It worked through weak salmon prices in 2025, with many producers still operating under margin pressure heading into this year. It worked through shipping disruptions in 2021 and again in 2024. What hasn't happened, at least not in the last decade, is a very strong El Niño, a shipping cost spike, and depressed salmon prices all landing in the same window. Right now, that's the direction the data points.

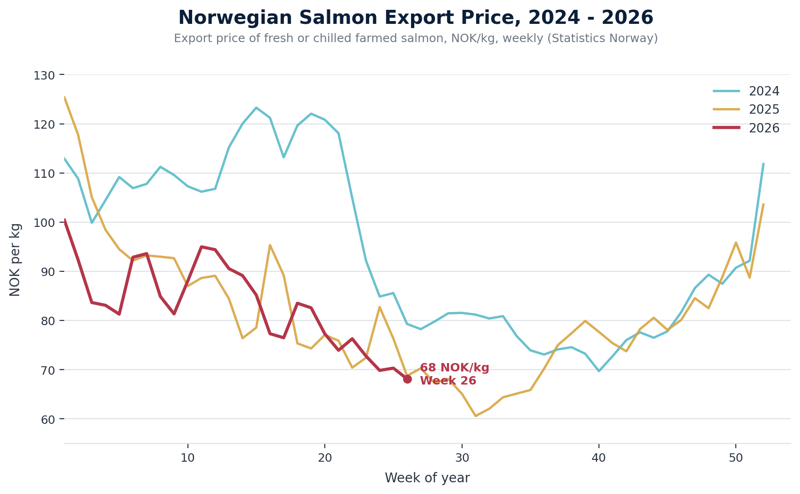

Norwegian export prices show how little room producers have to absorb a feed cost increase. Fresh salmon that fetched 120 kroner per kilo through much of spring 2024 has traded in the 70s for most of this spring, ending week 26 at 68 kroner. Prices in 2026 have tracked at or below 2025 levels for most of the year to date.

That combination is what makes this cycle harder to plan around than past disruptions taken individually. A company can build a contingency plan for a feed price spike. It's a different problem when feed costs, freight costs, and salmon revenue are all moving against you at once.

What's actually in a company's control

Obviously, nobody can control El Niño, salmon prices, or global container rates. What a farm or feed buyer can control (however) is how quickly they see a cost shift coming and how well their existing data supports a fast response.

That's the layer Manolin works in. Production planning models built on a farm's own history, treatment records, and environmental data give teams a clearer read on where cost pressure will actually hit, rather than reacting to a feed price increase after it's already locked into a purchase order. Reducing the time spent assembling reports from scattered systems means that time goes toward the decisions that matter when input costs and shipping costs are both moving: how much to buy forward, where to adjust stocking plans, and which sites can absorb margin pressure and which can't.

The volatility itself isn't new to the industry. What's different this time around is how many variables are converging at once, and that's exactly the kind of moment where a farm's own data, used well, is worth more than usual.